Prospectus

|  |

Joint Proxy Statement/Prospectus

MERGER PROPOSED—YOUR VOTE IS VERY IMPORTANT

Dear Shareholder:

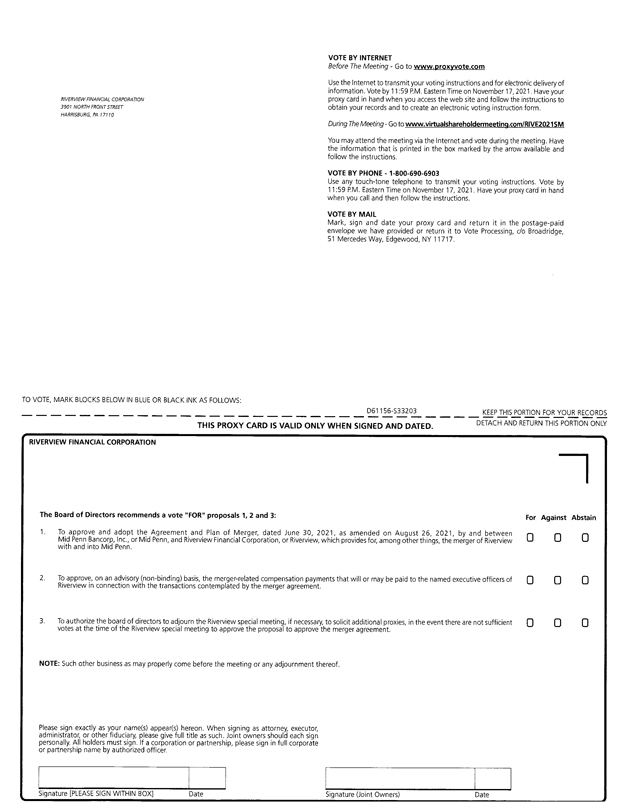

On June 30, 2021, Mid Penn Bancorp, Inc., or Mid Penn, and Riverview Financial Corporation, or Riverview, entered into a merger agreement, as amended on August 26, 2021, under which Riverview will merge with and into Mid Penn, with Mid Penn remaining as the surviving entity. Before we complete the merger, the shareholders of Mid Penn and Riverview must approve and adopt the merger agreement.

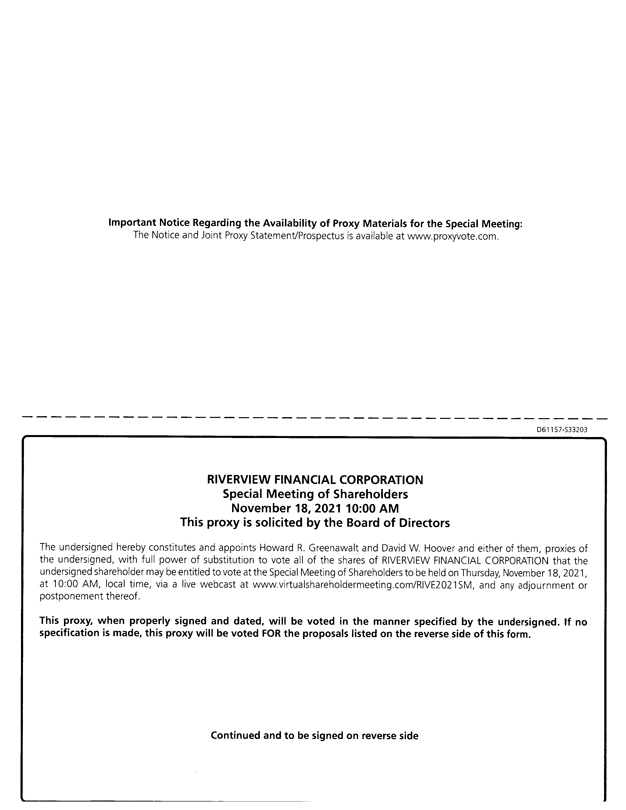

Mid Penn shareholders will vote to adopt the merger agreement and on the other matters described below at a special meeting of shareholders to be held virtually via live webcast at https://meetnow.global/MQZ7KWP at 10:00 a.m., Eastern Time, on November 18, 2021. Riverview shareholders will vote to adopt the merger agreement and on the other matters described below at a special meeting of shareholders to be held virtually via the internet at www.virtualshareholdermeeting.com/RIVE2021SM at 10:00 a.m., Eastern Time, on November 18, 2021. Information regarding how Mid Penn shareholders and Riverview shareholders can attend and participate in their respective special meetings of shareholders is included in the proxy card for the respective companies included with this joint proxy statement/prospectus.

If the merger is completed, Riverview shareholders will have the right to receive for each share of Riverview common stock they own 0.4833 shares of Mid Penn common stock. Cash will be paid in lieu of any fractional shares. The maximum number of shares of Mid Penn common stock estimated to be issuable upon completion of the merger is 4,524,639. Following the completion of the merger, former Riverview shareholders will hold approximately 28.2% of Mid Penn’s common stock.

The common stock of Mid Penn trades on the Nasdaq Global Select Market under the symbol “MPB” and the common stock of Riverview trades on the Nasdaq Global Select Market under the symbol “RIVE.” On June 29, 2021, which was the last trading date preceding the public announcement of the proposed merger, the closing price of Mid Penn common stock and Riverview common stock was $27.47 per share and $11.90 per share, respectively. On October 5, 2021, the most recent practicable trading day prior to the printing of this joint proxy statement/prospectus, the closing price of Mid Penn common stock and Riverview common stock was $27.89 per share and $13.28 per share, respectively. The market price of both Mid Penn common stock and Riverview common stock will fluctuate before the completion of the merger; therefore, you are urged to obtain current market quotations for Mid Penn common stock and Riverview common stock. Additionally, as described in more detail elsewhere in this joint proxy statement/prospectus, under the terms of the merger agreement, if the average price of Mid Penn common stock over a specified period of time decreases below certain specified thresholds, Riverview would have a right to terminate the merger agreement, unless Mid Penn elects to increase the exchange ratio, which would result in additional shares of Mid Penn common stock being issued.

The Mid Penn board of directors has determined that the merger is advisable and in the best interests of Mid Penn and the Mid Penn board of directors unanimously recommends that the Mid Penn shareholders vote “FOR” the adoption of the merger agreement and “FOR” the approval of the other proposals described in this joint proxy statement/prospectus.

The Riverview board of directors has determined that the merger is advisable and in the best interests of Riverview and the Riverview board of directors unanimously recommends that the Riverview shareholders vote “FOR” the adoption of the merger agreement and “FOR” the approval of the other proposals described in this joint proxy statement/prospectus.

Your vote is very important. Whether or not you plan to attend your shareholders’ meeting, please take the time to vote by completing and mailing the enclosed proxy card in accordance with the instructions on the proxy card. Mid Penn and Riverview shareholders may also cast their votes over the Internet or by telephone in accordance with the instructions on the Mid Penn or Riverview proxy card or voting instructions, as the case may be. We cannot complete the merger unless Mid Penn and Riverview shareholders approve and adopt the merger agreement.

You should read this entire joint proxy statement/prospectus, including the annexes hereto and the documents incorporated by reference herein, carefully because it contains important information about the merger and the related transactions. In particular, you should read carefully the information under the section entitled “Risk Factors” beginning on page 32. You can also obtain information about Mid Penn and Riverview from documents that each has filed with the Securities and Exchange Commission.

We strongly support this combination of our companies and join with the other members of our boards of directors in enthusiastically recommending that you vote in favor of the merger.

|  | |

| Rory G. Ritrievi | Brett D. Fulk | |

| President and Chief Executive Officer | President and Chief Executive Officer | |

| Mid Penn Bancorp, Inc. | Riverview Financial Corporation |

The shares of Mid Penn common stock to be issued to Riverview shareholders in the merger are not deposits or savings accounts or other obligations of any bank or savings association, and are not insured by the Federal Deposit Insurance Corporation or any other governmental agency.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved the Mid Penn common stock to be issued in the merger, or passed upon the adequacy or accuracy of this joint proxy statement/prospectus. Any representation to the contrary is a criminal offense.

The date of this joint proxy statement/prospectus is October 5, 2021, and it is first being mailed or otherwise delivered to Mid Penn shareholders and Riverview shareholders on or about October 12, 2021.

This document incorporates important business and financial information about Mid Penn and Riverview that is not included in or delivered with this document. This information is available without charge to shareholders upon written or oral request at either Mid Penn’s or Riverview’s address and telephone number listed on page i. To obtain timely delivery, Mid Penn shareholders must request the information no later than November 4, 2021 and Riverview shareholders must request this information no later than November 4, 2021. Please see “Where You Can Find More Information” on page 117 for instructions to request this and certain other information regarding Mid Penn and Riverview.